Thank you everyone for your attendance last Wednesday to our Rebalancing event where we pitched some decisions to be made on current holdings and heard some pitches from our CIO and some analysts on potential purchases!

Thank you everyone for your attendance last Wednesday to our Rebalancing event where we pitched some decisions to be made on current holdings and heard some pitches from our CIO and some analysts on potential purchases!

This is the ninth issue of the LSMIF newsletter. Please share with your friends and family and message in the Discord to participate and share a story!

US Companies face biggest decline in profits since Covid shutdowns: First-quarter earnings expected to fall 6.8% as inflation squeezes margins – June of this year, the US is in a medium-sized recession. Mark my words.

First batch of IPOs under new China listings rules surge on debut – Near triple-digit gains point to need for more reforms in country’s equity fundraising system, says experts

Yen slides as new Bank of Japan governor sticks to ultra-loose policy – Kazuo Ueda says negative interest rates and yield curve control remain appropriate for now

China escalates military drills near Taiwan and Japan – PLA aircraft carrier carries out 120 flight sorties in retaliation for Tsai Ing-wen’s US visit – The second the US collapses, Taiwan is being invaded by China

India boost investment along disputed border with China – New Delhi seeks to strengthen presence on ground as it vies with Beijing for influence in fraught region

Pay for FTSE100 chiefs rises by 12% despite cost of living crisis – Most upcoming executive salary increases are still below the average for workers after investor pressure

Fed fund futures show 80% probability of a 25 BP Fed Hike in May ! I think if Powell keeps his finger off the money printer for a while (which seems unlikely due to the yield curve) then they might avoid a huge recession

BRICS AGAIN! – Brazil, Russia, India, China and South Africa overtake G7 nations in global GDP to become more economically powerful – Take it in and enjoy the new world order!

China further increased the size of its gold reserves in March. The country purchased 18 tons, bringing their total to 2,068 tons of gold in total!

French President Macron says that Europe must reduce dependence on US dollar… he also makes a huge blunder basically saying leave China to take Taiwan… He’s cosying up big time!

The future is here! 95% of central banks are looking into the digitisation of their native currencies and with good reason! When you use a banking app now and send money or pay for things with money, it might seem instant to you but all you’ve sent is a digital IOU, the receiver gets a digital claim and the money takes about 3 days to crossover. That’s not very efficient, and while cryptocurrencies, like Bitcoin and Ethereum, literally solve this in a decentralised and pretty efficient way, it’s not good for business in the eyes of the government.

The digital yuan is already in place and being used nationally in China but it comes with an expiry date! Spend or lose out! Imagine having your bank account wiped just because you said something the government didn’t like (maybe just like this blog?). With CBDCs, this is a very real possibility. They could block your account, choose where you spend it, when you spend it. I don’t know about anyone else but I think I’m okay without…. They would have direct control over money but that’s quite good in a way. They already do and try to control it further through quantitative easing where they flood the economy with money and buy Treasury bonds and mortgage backed securities. They can also restrict the money through quantitative tightening which is this process in reverse, by selling off the assets. This is the stage we are in now.

The fact is, not many people trust the government (about 1 in 10 do) and whether we like it or not, this is the next stage. It is faster and better than traditional banking; middlemen like high-street banks will cease to exist in the way we know. They exist now to verify our transactions but the use of instant and verified transactions doesn’t leave much room for them. You could send and receive instant payments 24 hours a day and these transactions will settle instantly. Now that part is good but the potential control… I’m not sure. I know that Orwell (and Huxley!) are turning in their graves right now!

The unemployment rate is always at a cyclical low just a few months before a recession kicks in. The TMC Global Credit Impulse measures the amount of real-economy money printing for the 5 largest economics in the World. It now looks worse than just before the Great Financial Crisis (2008) and the Eurozone Debt Crisis; this doesn’t even account for the upcoming credit crunch.

Inverted yield curves mean Central Banks are disincentivising the flow of credit and choking the economy off, causing sharp slowdowns. The longer the curve inversion lasts, the more economic damage follows. The Fed will be forced to cut to ~1% but they will be too late…

The inverted yield curve looks at the interest rate on 10-YR Treasury bonds compared to the 2-YR bonds. When you buy a bond, the longer it takes for those bonds to return that money, the more money you can expect to make from them; this makes sense due to opportunity cost. If you wanted to borrow my money for 10 years, I would charge you a higher interest rate than if you wanted to wanted to borrow for 2 years as I’m taking on more risk. That’s how it works in a healthy economy. However, when the economy flips and we have high interest rates, if those rates are hurting the economy (like now), people have started to expect those rates to come down to re-stimulate the economy. Historically speaking, that’s very bad. The yield curve is so inverted, we haven’t seen it like this since the 1980s… Even if it corrects now, a recession cannot be stopped.

If and when the recession occurs, inflation will stay high and most likely go even higher. OPEC cutting oil production is bad for inflation. This is as the cost of energy accounts for 7.5% of CPI (inflation). Oil has already moved up in price in response to OPEC’s decision.

People took real mortgages to buy houses in the Metaverse, paid $1 million for JPEGs (NFTS are a bit more than that but simplistically I’ll say JPEGs) and thousands of unnecessary “tech workers” were paid $200k/year. A lot of people are about to get unemployed to fix that. Even McCarthy said to Wall Street: “You should worry about US Debt Ceiling”…. While a recession is technically two successive quarters of negative GDP growth, I think it’s safe to say a pretty sizeable recession is very very close. Even McDonald’s is laying people off… we know tech is the first to go with layoffs but to see a big consumer company with a reasonably low beta start to layoff, I think the odds are against the US.

If we get another rate hike, (80% likely) we can expect spillover to other parts of the economy. Real-estate is already feeling the heat, with billions of dollars in real-estate loans expected this year. In the next few years, ~$1.5 trillion of debt is due for US commercial properties before the end of 2025. Interest rates have increased drastically with inflation still rampant, meaning the interest payments on this debt is going to be a lot more expensive than was expected when this debt was created. Most of these loans are owned by smaller banks… and who just failed? Some pretty large banks (Silicon Valley Bank and Credit Suisse among those). If the large banks are failing, albeit for different reasons, with no bailouts like we had in 2008, how do we think it’s going to go when these smaller banks that will be owing a lot of debt in the next 3 years go under? Who will lend to these banks when they go insolvent and what will happen to property values? Morgan Stanley seem to think commercial real-estate prices could tumble up to 40%, which is rivalling the declines of 2008’s financial crisis!!!

The average person in America is only saving ~3.7% of their income which is the lowest since 1959… Wages haven’t kept up with inflation, meaning the average person has to take on more debt just to survive. The debt ceiling is getting crazy. The US have almost $1 TRILLION in credit card debt alone! Record credit card debt and record low savings with high interest rates…. I hope everyone is open to learning Mandarin because the new world order is going to get crazy in 2023. Late 2024 is really the latest we could see a recession in my opinion.

So much credit has been created that is unproductive and speculative… it energised the economy, now it will make it fall off the inevitable cliff. This is the sequel to 2008, and like all sequels, it will most likely be worse.

(not financial advice) I’m looking to buy bonds after the last interest rate hike (note: this is incredibly difficult to time well), I’m buying more exposure to emerging markets, like India and especially China. I’m buying more gold and large cap. low beta companies like Unilever and PepsiCo. (PLEASE) Do not copy this as I’m not a professional.

As always, thank you for your participation and attention.

Many Thanks,

Aymen Retibi

Chief Investment Officer

LSMIF Management

This is the eighth issue of the LSMIF newsletter. Please share with your friends and family and message in the Discord to participate and share a story!

Credit Suisse chair apologises to investors at bank’s final AGM – Executives had been braced for protests from Swiss citizens outraged at takeover by UBS – One thing I find hilarious is his Lehmann’s quote: “It is a sad day. For all of you, and for us” He has to remind himself that he’s supposed to be sad and pretend he lost money like the average person.

Sterling rises to highest level in 10 months.

Blackstone fund hit by $4.5bn of withdrawal requests despite property pitch – March conference on sector opportunities fails to stem efforts to pull money out of BREIT. This is interesting because Blackstone has attracted a lot of confidence recently, is this the sign of a general market decline?

Donald Trump to be arraigned in New York criminal case – Former president expected to enter ‘not guilty’ plea as he makes his first appearance in hush-money case – The main man himself! If he makes a come back from this it’ll blow my mind

L’Oreal buys Australian luxury cosmetics group Aesop in $2.5bn deal!

JPMorgan executives joked about Jeffrey Epstein’s behaviour, US Virgin Island alleges – Filing comes in litigation accusing the bank of benefiting from its relationship with the late sex offender – I mean where there’s money, there’s crime. Where there’s a wealthy banker….

Russia confiscates passports of senior officials to stop defection – Kremlin tightens Soviet-era travel restrictions in ‘sensitive’ areas – Nothing spells confidence in your government like them taking your passport so you can go against their unjust war!

Virgin Orbit files for bankruptcy protection in US – Richard Branson’s rocket launch spin-off has already ceased operations and cut 85% of workforce – Branson’s actually having a stinker! The space industry isn’t for everyone is it Branson or Bezoz?

OPEC+ makes surprise 1 million-barrel cut in new inflation risk! This favours Russia, with Saudi Arabia and Russia lead the charge with a -500k BPD cut!

BRICS (Brazil, Russia, India, China and South Africa – the leading emerging markets!) are developing a new form of currency! This is the dollars biggest threat!

Gold is very important, and it used to be to the Dollar. It was the standard of trade between countries and exchange of value for currency valuation. The US pivoted to a lack of reserve value for the dollar and started to print more money with no “worth” behind it. This shift happened as they essentially defaulted on their overspending with not enough gold to back up the cash they had printed. So Nixon was forced to do this in 1971 to save the dollar.

With no gold to hedge its value, the constant printing and spending of the dollar has led to its gradual devaluation as we know it, and this rhymes with the decline of previous empires, such as the Dutch and the British. This lack of hedged value, coupled with creating more money and printing it endlessly devalues the currency more and more overtime, making the price of everything go up in response (inflation). A rule of thumb, when central banks print a lot, buy more stocks and commodities as these values will rise while paper money falls.

With over 80% of US dollars printed in the last 5 years, we are entering a period unbeknownst to most of us in terms of size and speculative decline. The dollar may rise and fall short-term, but the long-term outlook looks to be bleak for the dollar.

The US has had 3 sizeable boom and busts since the 90s and this looks set to happen again.

We are close to entering the crossover to Chinese power and currency dominance!

I’m using these graphs by Ray Dalio as a metric for time frames and also the position the dollar is at. I hate to say it but the US is in the decline phase.

The dollar positioned itself as the leader for trade of petrol; control the black gold, control the world. Now the petro-dollar is starting to weaken excessively as OPEC pivots to control petrol prices and outflows as well as using alternative currencies or means of trade between one another to offset the power of the dollar. China is creeping in areas that the US has failed in. They have cemented themselves in Nigeria’s infrastructure and oil production and they love it!

The creation of OPEC itself and now their chokehold on oil productions and therefore prices just highlights the decline of the US’ power. China and Russia have also been buying substantial amounts of gold for trade between them and for the creation of their new currency with has support from large emerging markets like Brazil. The creation of a new currency for trade, backed partly by gold, oil, and the yuan is seemingly on the horizon. Jerome Powell of the US’ Fed himself said there is the possibility of more than one global reserve currency. I think this is a substantial threat that we have never seen before.

I just want to highlight this graph. China is really playing its cards well in terms of the 8 metrics which contribute to the rise (and fall) of empires. Education, innovation and technology, competitiveness, output, trade, military power, financial centres, and reserve status. The US education system, like the UK, is stagnating leading to a technology stagnation (eventually). Look at China. They dominate in the majority of these areas minus reserve status and military power. They even limit game time, screen time, and the content on TikTok if it is not educational!

It’s hard to say that the US hasn’t started to lose its global grip and dollar devaluation and therefore a global overvaluation. Dollars held around the world by central banks have been declining since 2008 and continue to do so. This does not mean the yuan is suddenly a gem. It’s not. China holds a lotttt of US treasury bonds and still has to deal in dollars and does hold a decent amount. They would not benefit off a huge immediate decline. But… they would benefit from a 15-20 year transition where they position themselves perfectly to watch it crumble and pick up the pieces.

Russia has recently been crippled when its dollar wallet was frozen in retaliation but its alliance with China and mass oil output, means it can sell oil and trade in currencies that aren’t the dollar keeping it charging forward. Most countries are following suit, dropping the dollar when oil trade is in the picture. Petro-yuan or gold, not petro-dollar….

I see the Ukraine war and potential Taiwan war as catalysts for internal and external shifts within and between countries, in some part amounting to the end of the dollar. Which, as I said, if it happened now, would massively harm China and the world.

So, the dollar is still relatively strong and will see some upside…. for now.

Please shoot me a message if you’ve read this far on what you enjoyed/didn’t enjoy and with any recommendations etc! I’m going to start looking at trading pies on Trading212 so if you have any you’d like to be featured please shoot me a message!

As always, thank you for your participation and attention.

Many Thanks,

Aymen Retibi

Chief Investment Officer

LSMIF Management

This is the seventh issue of the LSMIF newsletter. Please share with your friends and family and message in the Discord to participate and share a story!

L&G chief says Uk levelling up policy is “failing” – Sir Nigel Wilson is pushing for policy change to encourage investment outside the capital; he notes we aren’t building enough affordable housing, social housing or build-to-rent housing. He states old assets will decrease value and sees modern investment and properties to be more relevant.

First Citizens to buy failed Silicon Valley Bank: Family-owned company’s acquisition of tech-focused lender’s deposits and loans follows sale of collapsed Signature Bank

Hedge funds scale back bets against Scottish Mortgage – Investors close short positions in expectation that share price may be nearing bottom!!! This is massive news for the fund, we have the opportunity to reduce our average PPS massively catching the bottom and riding the wave of nearly +50% back up to levels seen at the time of original purchasing! Watch this space closely.

Money Market funds swell by more than $286bn as investors pull deposits from banks: Goldman Sachs, JPMorgan Chase and Fidelity benefit from big inflows and turmoil in financial sector

UK higher education applicants to rise to 1mn a year by 2030, warns UCAS – University application service calls for targeted effort to increase places for students – This is quite funny as it just shows how much university is actually a business and we are just consumers. To benefit off this, investing in housing companies that work closely in student-housing or have large projects planned in regions of high university applicants would be a wise decision.

Wetherspoons hit by ‘ferocious’ inflation – UK pub chain ekes out small profit but sales still lag pre-pandemic level. The irony in this is I’m sat in spoons as I’m writing this and now I’m exploring the options to short sell JD Wetherspoons PLC.

February inflation surpass seals BoE rate rise: Interest rate rises went up by 0.25% to a total of 4.25% and with inflation still >10%, I still think we have one or two more rises on the way. Although, inflation should cool more rapidly before summer

Fed officials double down on rate rise decision citing high inflation – Like the UK, the Fed pressed ahead with a .25% rate rise up to 5% even amid the financial sector wobble. What is worrying to me is in most countries we are at rates that are equal to or higher than 2008, banks are taking hits and they are still raising rates because they’ve been printing money like mad men. More money is being printed soon in the US so inflation will run away. The US dollar is overvalued. I stand by this. >80% of all US dollars in existence have been printed in the last 3-4 years. Yikes.

(LAST 3 MONTHS) (1) I have been day trading gold quite a lot recently. I expect it to drop slightly from current levels before a marked increase up to highest regions marked by (2). Confirmation (3+4) shows that we can expect gold to rise from now so I will probably enter a large long position. (4) I’m expecting a slight drawdown before a large turn in positive momentum (+5% or more).

(LAST YEAR) (1) I just want to highlight on the yearly, the very likely movement for Gold. A drawdown then a big move up early summertime. (2+3) Confirm this drawdown.

(LAST 3 MONTHS)(1) The dollar is in a prolonged downwards movement with the bottom marked by the orange zone and shown in the -1.23% expected drop. (2+3) Suggests the downwards momentum has begun and will continue to drop further.

(LAST YEAR)(1) To me, I’m seeing drawdown before some upside but I may be wrong in thinking it’ll be sizeable. It seems more likely it’ll look like a dead cat bounce. Where it bounces up a bit then crashes back down where I see the dollar likely moving. (2+3) Sorta confirms this.

(LAST 3 MONTHS) (1) I expect an -11% or more drawdown for Bitcoin. Binance is being sued and I’ve read the court charge papers and it does seem quite bad. I’m expecting a retest of regions with more support. I will be entering a large short position. (2+3) These just confirm the downwards momentum and scale of the -10%. I do see some upside in the form of a relief rally before more of a drawdown that I’m expecting.

(LAST YEAR) (1). Just want to highlight the path that is most likely for Bitcoin IMO with (2) showing a pretty bad case but ultimately, very real, possibility. (3) Just confirms we’ve had our local top and will retest a new bottom. (4+5) Now these are just scary. This is showing that we are due some heavy downturn so my short positions are about to get a lot larger. However, I do so a short term relief rally upwards before this substantial drop.

As always, thank you for your participation and attention.

Many Thanks,

Chief Investment Officer

LSMIF Management

This is the sixth issue of the LSMIF newsletter. Please share with your friends and family and message in the Discord to participate and share a story!

Janet Yellen to signal further US support for deposits at smaller banks: Treasury secretary to defend ‘decisive and forceful actions’ by regulators to avert broader crisis… To me this is having a broken leg then stubbing your toe and only focusing on the toe. Yes it hurts but it is not your only problem. (Weird analogy I Know) The point is inflation is going to runaway again and GDP growth will slump, markets will tumble and again, they are only focusing on saving banks. 2008. That is all.

Nato expects allies to agree 2% defence spending “as a minimum” – If you own Lockheed Martin, Raytheon Technologies, General Dynamics, or any defence stock, enjoy your money because these stocks are going to do well with this announcement. A little known fact about Nato defence spending agreements are that the US get a large proportion of these contracts as a standard of the agreement.

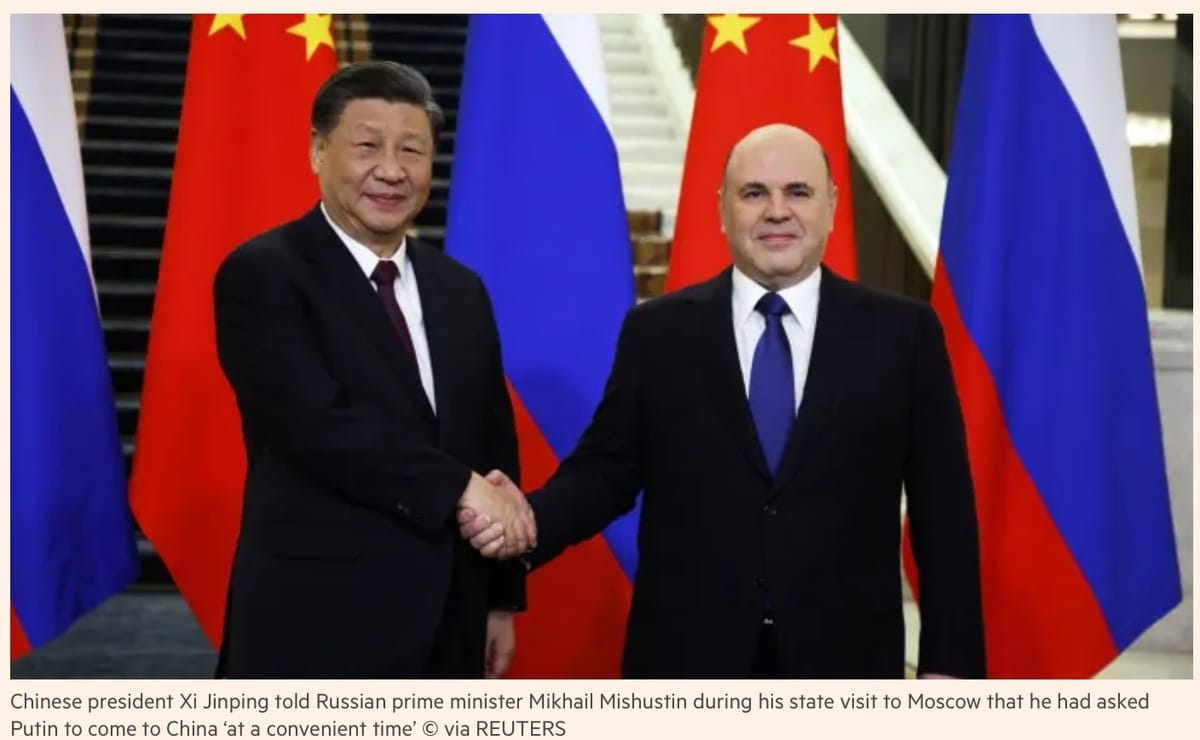

Xi Jinping invites Putin on state visit to China: I mean if this isn’t terrifying I’m not sure what is. The cosy relationship between Russia and China with their increased gold-buying, moving away from the dependency on the dollar is really pivotal in the sense of what is to come.

Google launches Bard chatbot to rival OpenAI’s ChatGPT: Tech giant seeks to make up lost ground in race to commercialise generative AI… I find this pretty exciting to be honest because when the big hitters all get involved they essentially spark an arms race and we get some very ingenious tech out of it. Watch this space closely.

Scottish Mortgage chair to step down in shake-up: McBain exits after rare public row over corporate governance… The fund owns some and seeks to buy more of this stock so this is something we should keep our eye on for sure.

UK public borrowing rises on energy support schemes: February figures of £16.7bn is higher than expected… Again, not to be that guy but 2008.

B&Q owner Kingfisher reports 20% drop in profits: They see profits falling even further this year so I might look to short this stock if I’m honest.

VOTING POLLS:

Below is two polls on some ERR companies chosen to be purchased and sold, please have a look and vote! This does not reflect all choices to be made, just some and is to double check decisions made in the Wednesday Meeting.

As always, thank you for your participation and attention.

Many Thanks,

LSMIF Management

This is the fifth issue of the LSMIF newsletter. Please share with your friends and family and message in the Discord to participate and share a story!

SVB Meltdown:The UK arm of SVB was sold to HSBC for £1 which is pretty hilarious. The US (main arm) is now in the process of government “bailouts” but this really begs the question, who’s next? Everyone seems to feel this is relatively contained but Credit Suisse’s stock price wobbled and a few other big bank’s have felt the pressure. Apollo, Blackstone and KKR among private capital groups eyeing SVB’s portfolio.

US consumer prices come in at 6% at tricky time for Fed amid SVB fallout: Data comes as central bank contends with broader concerns about how rising rates may have affected lenders – A rate rise follow through this week is still likely but now more risky…

ChatGPT maker OpenAi unveils new model GPT-4 – “most advanced system yet” – It is x500 times more powerful than 3.5…. They claim it exhibits “human-level performance” – It is multimodal so can accept both image and text forms and has many other apps embedded, such as Duolingo, Khan Academy and others.

SVB collapse forces rethink on interest rates and hits bank stocks: Two-year US Treasury bond yields record biggest one-day drop since 1987

Argentina’s inflation rate tops 100% for the first time in three decades!!!

Celadon becomes first UK medical cannabis group to win right to sell in Britain

Meta axes further 10,000 jobs in fresh round of cuts – strives to improve “efficiency”

China set to tighten grip over global cobalt supply as price hits 32-month low: Share of global output expected to reach 50% over next two years

UK Economy: IMF forecasts it will be the worst-performing large advanced economy this year. annual growth rates have more than halved since 2007-09. The economy is no bigger than before the pandemic and a recovery is not expected until 2026 (at the earliest) according to the BoE. Brexit slammed the brakes on UK investment. Now we are plagued by high inflation with no end in sight and a cost of living crisis amongst endless other things… We still aren’t at peak interest rates and loom in the limbo of a sizeable recession.

Credit Suisse to borrow up to $54B from Swiss central bank: Troubled lender’s shares rebound after Wednesday’s plunge of as much as -30%!

Jeremy Hunt’s giveaways in his budget announcement will have a marginal impact on UK growth, says watchdog: Office for Budget Responsibility says the country’s long-term growth prospects look no better than last November – while this free childcare and short-term budget balance seems good, it really won’t stimulate or save the economy as proposed

As always, thank you for your participation and attention.

Many Thanks,

Aymen Retibi

Chief Investment Officer, LSMIF Management

This is the fourth issue of the LSMIF newsletter. Please share with your friends and family and message in the Discord to participate and share a story!

Our Team, ready to present in the SMIF Competition in York

Matteo De Rossi (CEO) giving a presentation to 150 students.

Also, I’m still recruiting participants for my dissertation. If you’re interested in why losses are more “painful” than relative gains can be “pleasurable”, have an interest in game theory, or just generally have a spare second, please give my study a go!

As always, thank you for your participation and attention.

Many Thanks,

LSMIF Management

This is the third issue of the new LSMIF newsletter. Please share with your friends and family and message in the Discord to participate and share a story!

As always, thank you for your participation and attention.

Many Thanks,

LSMIF Management

This is the second issue of the new LSMIF newsletter. Please share with your friends and family and message in the Discord to participate and share a story!

Again, thank you for your participation and attention.

Many Thanks,

LSMIF Management

This is the first issue of the new LSMIF newsletter. Please share with your friends and family and message in the Discord to participate and share a story!

First ERR on 22nd Feb. This marks the first purchases and rebalancing of the portfolio marking a new stage of the fund.

In terms of Management’s timeline and plan for the fund, we have achieved a lot together compared to last year. We have incorporated new communication strategies, remodelled training and feedback for tasks, and created a more democratic style for decision making and portfolio decisions.

“Being involved in the LSMIF has been a unique experience so far. The LSMIF management team provided guidance and support to complete all training tasks and the final Equity Research Report. Since I learned how to read and analyse financial data, I was confident about managing time and information effectively.

The past four months, I had the chance to work on Lloyds Banking Group PLC profile, while I discovered the macroeconomic factors, inflation that affect the financial sector and banking industry. I feel privileged enough to join the fund and have high expectations in the investment banking sector in the future. I hope more and more students join the fund and enhance their analytical and critical capabilities.” – Athanasios Tsanaktsidis

If any of you, whether Trainee or Senior, have anything you would like to share or add to next week’s newsletter, please feel free to reach out and message Management.

As always, thank you for your effort and participation!

Many Thanks,

Powered by WordPress & Theme by Anders Norén